In less than three months, Yearn Finance has grown from a relatively obscure credit aggregator to one of the main driving forces behind the $ 670 million DeFi market (over $ 1 billion at its peak) and is at the center of the hottest trend in the industry today – Yield Farming. crop farming). Yearn dominated Yield Farming so convincingly that some presented its token, YFI, as the Yield Farming Index (Yield Farming Index). But with such a sudden rise, it’s worth pondering the complex issues of value, impact, risks, and opportunities for Yearn in the future. It’s Time To Reveal One Of The Most Complex DeFi Protocols On The Market.

The birth and flowering of YFI

Until July 16, Yearn was a simple DeFi lending aggregator designed to optimize user returns. He had $ 8 million in assets under management, and since launch in January he earned a combined 10.58% per annum of the profits of his liquidity providers. But most importantly, he didn’t have a token.

That all changed the next day, July 17th, when yearn.finance founder André Konye published an infamous blog post titled “YFI”. In an effort to transfer control of the yearn.finance protocol to its users, Cronje has developed a plan for users to manage YFI by providing liquidity to Curve and Balancer pools. This may have been the first truly honest launch in many years that Cronje did not allocate YFI tokens to himself, giving up any rounds of funding, advisor tokens, premines, or whatever. All YFI tokens were distributed to users of the yearn.finance protocol.

A couple of months later, the supposedly “completely useless token” is worth $ 670 million and runs an “industrial scale agricultural machine” the size of $ 770 million (At its peak, almost a billion dollars). And he prints money for token holders worth about $ 20 million a year.

Industrialization Yield Farming

A long time ago (in fact, about three months ago), Compound launched its liquidity mining program and launched the speculative hobby that many have dubbed The DeFi Agrarian Revolution. Simply put, liquidity mining refers to the process of distributing tokens to users to use the protocol. The goal of liquidity mining is to distribute control over the protocol and drive its adoption. The community coined the term “Yield Farming” by analogy between users who invest in a protocol to obtain tokens with farmers working in the fields to harvest.

In the weeks after Compound mining launched, Yield Farming was pretty straightforward. You invest your capital in one of several protocols that offer incentives in exchange for liquidity and start earning tokens. This first phase of Yield Farming was similar to that of manual farmers. Users needed to define and understand each strategy before manually entering capital. But as more protocols launched liquidity mining programs and Yield Farming became more complex, the process became more and more time consuming for many users to participate. In addition, when gas prices rose sharply due to the congestion of the Ethereum blockchain, many small “farmers” stopped doing Yield Farming. That all changed when yearn.finance launched v2 (second version) of his protocol, introducing yVaults.

The most effective way to think about yVaults is to imagine a two-way market where capital providers are on one side and policymakers on the other. Strategy authors allocate capital to users, and capital providers choose which strategies they want to use. Strategies automate Yield Farming for users. With the launch of yVaults, potential farmers can now simply deposit their funds with yVault and their capital will be automatically allocated to the best strategies available. The vaults not only reduce the risk faced by users trying to understand the various possibilities of Yield Farming, but also allayed their fears about gas charges by sharing them with other capital providers in the pool. As a result, Yearn.finance has grown to become the largest Yield Farming venture in the industry, doing what used to be a business that only experienced users could participate in. It took more than ten thousand years for humanity to move from agrarian to the industrial age. It took DeFi a couple of weeks..

Cash flow machine

YFI is not an easy project. It has core products Earn (lending optimization) and Vaults (Yield Farming optimization), as well as many different products in its roadmap in insurance, stock trading, leverage, venture capital and liquidation. In addition, this tokenomic model is still in development stage with the help of consulting firms Delphi Digital and Gauntlet. However, it is important to understand how YFI is currently making money from its two main products, Earn and Vaults, as they can provide insight into its future (economically).

The economy is simple. YFI charges a gas subsidy (productivity) fee of 5% of the capital it manages, and a withdrawal fee of 0.5% if users withdraw their capital. Withdrawal fees apply to both Earn and Vaults products, while performance fees apply only to Vaults products. In particular, with vaults, a performance fee is charged each time a “harvest” occurs (selling a processed asset back for the underlying asset). After adoption YIP-36, which determined that Yearn would use part of the system rewards (commissions) as operating capital, 100% of the system rewards were sent to his treasury with multisig signatures. The YIP specifies that the Treasury must maintain a buffer of the equivalent of $ 500,000, with any surplus remuneration allocated to YFI placed in a management pool.

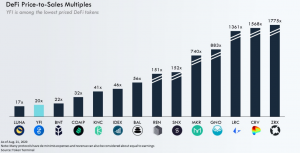

Within a week of implementation, the Treasury has already amassed over $ 463,000 in revenue, which is just over $ 21 million in annual terms. With a market capitalization of $ 390 million at the time, this implies a price-to-sales ratio of about 20 times, which for all intents and purposes can also be viewed as a price-to-earnings ratio, given that the protocol has no costs beyond what it gets from its treasury.

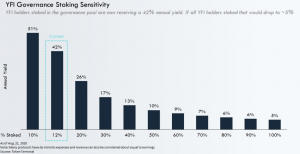

The inverse YFI price-earnings ratio means that if all YFI holders made a stake, they would receive ~ 5% annual return (only YFI holders participating in the corporate governance pool receive cash flows). Since the pool currently hosts about 12 % YFI (large percentage YFI is placed in other pools), YFI members receive ~ 40% annual return, which implies a PE ratio of 2.4 times. It is best to understand these ratios as a range. Currently, YFI holders participating in the management pool receive ~ 40% annual return, but if everyone stakes, they will receive ~ 5% annual return. 5% can be seen as a cap based on the current price and profit per token.

Market movement

Yearn’s Yield Farming strategies were so successful that they started to move the markets in earnest. It is important to understand that Yearn’s Vaults not only automates user strategies, but also aligns those strategies. So, instead of some users selling tokens when they process them, and some users holding tokens because they prefer to withhold or not pay for gas, all yVault users do one thing. And when that one thing is the systematic sale of fermented tokens, it can have a significant impact on the underlying fermented tokens given Yearn’s assets under management. The most recent example is CREAM, a decentralized lending protocol built on top of Compound, which recently launched liquidity mining. From the moment launch YFI vaults, the vault systematically grew CREAMs and sold profits for additional YFIs. Basically, the strategy benefits from CREAM speculators who list newly acquired CREAM tokens and redirect them to YFI.

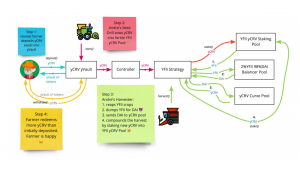

The yCRV repository below demonstrates how this process looks from the inside. There are some differences from this repository, but the general logic is the same. Replace yCRV with YFI and YFII with CREAM and the figure will look very similar.

As yVaults adoption grows, Yearn will collect an increasing percentage of the total revenue from all of the most profitable “farming opportunities” as long as the trend continues. Then the question arises, is it sustainable.

Sustainability

The main reason Yearn can generate such a large cash flow right now is because the yield is very high. Yields are high for a reason. It is high because it is supported by a speculative fascination with protocols with liquidity mining programs. The reason why “farmers” can receive “yields” in three-digit or more percentages is because speculators continue to buy new tokens on exchanges. Simply put, speculators pay for the “crops” that the “farmers” receive.

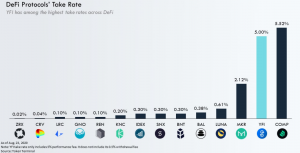

It is unclear how long the Yield Farming craze will last. This may well continue beyond the next year, or it may end overnight. However, once interest subsides, token holders will need to find more sources of money. This could be due to either an increase in AUM to compensate for lower “yields” or additional products to provide alternative sources of income for the Yearn system. Equally important for YFI token holders is Yearn’s current usage rate. Yearn’s 5% performance fee means the highest utilization among all DeFi protocols. The commission may well be justified given the value Yearn provides capital providers, but this is not a guarantee. Even Cronje himself believes that YFI token holders cannot simply receive rent from capital providers..

In addition, under the current system, Yearn does not pay for strategy authors. It’s as if the asset management company didn’t pay its portfolio managers. To the extent that Yearn acts as a decentralized asset management platform (which some compared to a nondirectional / arbitrage-driven automated control platform), it will eventually have to compensate the strategy makers, leading to higher costs.

YFI perspectives

Perhaps there are no projects, more suitable to reflect the growth of Yield Farming than YFI. YFI’s short-term Common Marketplace is the Yield Farming Common Market, which currently provides $ 7.3 million in liquidity rewards on a daily basis. This implies an annual rate of $ 2.6 billion and the strongest tailwind for YFI..

However, while YFI is currently the leader in Yield Farming, it is not the only one fighting for the yield cake. Not only a few (often dubious) YFI forks have hit the market, but also new Yield Farming aggregators such as APY.Finance, and asset management platforms such as Set V2, which will increase competition. Plus, as mentioned earlier, the current payoff from Yield Farming won’t last forever. Speculators will eventually stop buying as many new tokens, leading to lower yields. While the successful launch of Yearn’s planned insurance, exchange-traded products, leverage and liquidation products could diversify YFI’s revenue streams and provide option value for YFI holders.

YFI remains one of the most exciting experiments in decentralized governance to date. YFI’s Fair Launch has created a large, diverse and enthusiastic community of people very interested in the success of the protocol. Thanks to Cronier’s professionalism and leadership, Yearn’s product release rates are impressive. There are very few protocols launching new products as quickly as Yearn. However, while Yearn is doing relatively well at this point, challengers are entering the market, and Yearn is about to launch many new products, the risk is far from zero. The coming months will show if this nascent community can continue its magic and benefit all stakeholders.